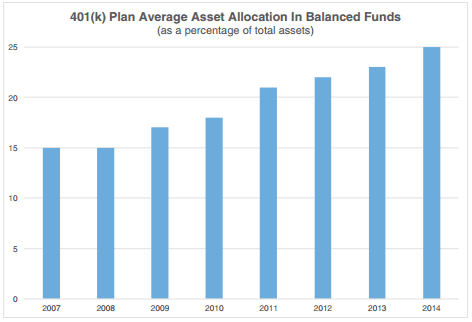

Retirement plan assets are becoming more “balanced.” Over the past several years, 401(k) participants have increased their overall allocation to balanced funds. According to data analyzed by the Employee Benefit Research Institute (EBRI) and the Investment Company Institute (ICI), the percentage of assets in balanced funds within 401(k) plans has been steadily climbing from 15% at the end of 2007 to 25% as of year-end 2014.

Source: Tabulations from EBRI/ICI Participant-Directed Retirement Plan Data Collection Project. Target date funds are included in this balanced funds category by EBRI and ICI.

The EBRI/ICI research defined balanced funds in their research as funds that invest in both stocks and bonds and classified them into two categories:

- Target date balanced funds

- Non-target date balanced funds including asset allocation and hybrid funds

In fact, nearly 40% of plan participants had more than 80% of their assets in balanced funds as of the end of 2014. In this article, we take a look at the primary factors driving this increase.

The Impact Of The Default Option On Allocation

When introduced in 2006, the Pension Protection Act encouraged both the use of auto-enrollment in retirement plans and allowed for a percentage of retirement assets to be automatically invested in a “qualified default investment alternative,” which for the first time included target date and non-target date balanced funds.

As a result, this encouragement of auto-enrollment successfully raised plan participation rates. In fact, for plans that offered autoenrollment, participation rates averaged nearly 90% at the end of 2015 compared with a less than 50% participation rate for plans without auto-enrollment.*

In addition, with the introduction of balanced funds as a “qualified default investment alternative,” allocations to balanced funds in retirement plans increased. Younger plan participants, in particular, were increasingly invested in balanced funds. EBRI/ICI research revealed that newly hired employees in their 20s were more likely to have higher concentrations of target-date and non-target-date balanced funds than their newly hired older co-workers. In fact, nearly 56% of participants in their 20s had more than 90% of their account balances invested in these funds compared with less than 51% of participants in their 60s.

Balanced Funds – Understanding The Trend

What this trend reveals is that younger investors seem to have accepted the default balanced fund options provided in their retirement plan, rather than proactively selecting their own mix of stock and bond mutual funds. In essence, they are comfortable delegating their asset allocation decisions to retirement plan investment professionals.

Interestingly, the trend in auto-enrollment and balanced funds has also led to an overall increase of plan participants’ allocation to stocks. In fact, more retirement accounts held equities at the end of 2014 than before the financial crisis in 2007, with more than 90% of participants holding some percentage in stocks, according to the EBRI/ICI data.

ABG’s 3(38) Solution – More Timely Than Ever

With this increased allocation to balanced funds as a result of the rise of auto-enrollment and the acceptance of balanced funds as a default option, participants are showing an overall willingness to delegate their asset allocation decisions to retirement plan professionals. Now more than ever, when it comes to the appropriate selection of investment options for a retirement plan, expert guidance for plan sponsors is key.

With this in mind, be sure to take advantage of ABG’s 3(38) investment management solution for retirement plans. Our team researches and screens the broad universe of mutual funds with the goal of providing a comprehensive yet manageable range of investment options to plan sponsors for inclusion in retirement plans. Contact your local ABG representative to learn more.

*According to a T. Rowe Price study